Cognitive Strategies for Retaining Historical Time within the Institutional Logic of Risk Distribution

Development of the Old and Young Thinking Framework and the Investor–Entrepreneur Cognition Model

Abstract

This paper presents a philosophical and systemic investigation of capital as a mechanism for retaining historical time.

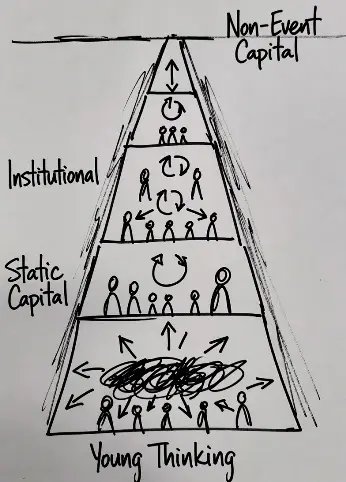

Within the proposed framework, capital is understood not as a collection of financial assets but as a hierarchically organized system of cognitive regimes differentiated by their temporal horizons: from event-driven reactivity (Young Thinking) to intergenerational stabilization (Static Capital) and the ultimate form of strategic continuity (Non-Event Capital).

The central hypothesis of the study is that the stability of large-scale social systems is explained not by the existence of centralized control, but by the asymmetry of cognitive regimes and by differences in the ability of actors to retain temporal horizons and redistribute systemic risk.

Particular attention is devoted to a cognitive theory of risk based on the distinction between Event-based and Distribution-based modes of cognition, as well as to the mechanisms of Risk Reconfiguration, through which localized risks are transformed into distributed systemic costs.

Within this framework, inflation is interpreted not merely as a macroeconomic indicator but as a mechanism for reallocating volatility across different structural layers of the economy.

The paper further introduces the concepts of Cognitive Buffer Zone and Existential Risk Offloading, which describe institutional mechanisms for reducing vulnerability through the transfer of risks to peripheral levels of the system.

Methodologically, the study relies on a philosophical reconstruction of institutional structures using OSINT-based analysis, data on trusts and family offices, as well as macroeconomic and corporate sources.

At the same time, it is emphasized that the categories employed throughout the paper constitute analytical abstractions and should not be interpreted as evidence for the existence of a centralized actor of global governance.

As a result, capital is interpreted as a form of organizing historical duration, while power is understood as a function of the capacity to retain and asymmetrically distribute time, risk, and uncertainty within complex institutional systems.

Keywords: cognitive regimes; historical time; capital theory; risk distribution; institutional theory; systemic resilience; philosophy of economics.

1. Introduction: Strengths and Weaknesses of the Framework

1.1. Cognitive Regimes for Retaining Historical Time

One of the central ideas of this paper is that capital should be understood not merely as a collection of monetary resources, but as a regime for retaining historical time.

Within this perspective (Table 1), a basic typology of cognitive-temporal regimes of capital is introduced:

| Regime | Temporal Horizon | Cognitive Specificity |

|---|---|---|

| Young Thinking | Event | Reactive processing of local volatility and event-driven shocks |

| Institutional Thinking | Cycle | Procedural reproduction of rules and coordination mechanisms |

| Static Capital | Generation | Intergenerational preservation and protection of structured assets |

| Non-Event Capital | Historical Duration | Complete autonomy from the event-driven and media logic of the system |

Within the proposed model, power is defined not by the volume of resources controlled as such, but by the capacity to maintain a longer temporal horizon, distribute risk across different layers of time, and ensure the reproduction of strategic orientations under conditions of uncertainty.

In its limiting formulation, capital ceases to be merely an economic category and becomes a form of organizing duration. Power, accordingly, is transformed into a function of a system's existential capacity to retain the future within the structure of the present.

Let us assume that the global capitalist system possesses neither subjectivity, nor centralized will, nor an anthropomorphic structure of governance. Both conspiratorial models of personalized control and radically reductionist models of entirely impersonal self-regulation are excluded.

Instead, a weaker yet analytically robust hypothesis is proposed: historical continuity emerges as a result of asymmetries between cognitive regimes, within which different actors possess unequal capacities for retaining temporal horizons and redistributing systemic risk.

The key objective of this study is not the analysis of inequality as such, but the construction of a cognitive theory of risk based upon the distinction between Event-based Cognition and Distribution-based Cognition.

In contrast to:

| Analytical Perspective | Core Assumption |

|---|---|

| Exploitation Reductionism | Critical tradition: the nature of capital is reduced to redistribution and struggles over the appropriation of surplus value. |

| Efficiency Reductionism | Liberal tradition: capital is viewed as a mechanism for maximizing aggregate social welfare through market processes. |

| Procedural Institutionalism | Coordination model: emphasis is placed on rules of the game, procedural stability, and the temporal persistence of institutions. |

the present work shifts the analysis toward the domain of cognitive processing of uncertainty and the temporal architecture of subjectivity.

Within this framework, inflation ceases to be interpreted solely as a macroeconomic indicator and is instead understood as a mechanism of Risk Reconfiguration—the systemic redistribution of volatility across different layers of the structure.

At the same time, two additional concepts are introduced:

- 01. COGNITIVE BUFFER ZONE: A buffering layer that filters out market noise and preserves the integrity of decision-making processes from short-term emotional and informational disturbances.

- 02. EXISTENTIAL RISK OFFLOADING: A mechanism for transferring systemic risks to external layers of the system, thereby ensuring the "immortality" of the core asset structure.

These concepts describe the transformation of localized risks within the system's core into distributed costs borne by peripheral layers. At this level, the analysis intersects with systems theory, complexity science, and contemporary theories of distributed risk management.

1.2. Analytical Assumptions and Limitations of the Model

It should be emphasized that several of the concepts employed throughout this work represent analytical abstractions and philosophical-systemic assumptions rather than empirically verified claims regarding the existence of a centralized subject of global governance.

In particular, the interpretation of large asset-management structures (BlackRock, Vanguard, and State Street) does not imply the existence of a unified coordinating center. They are examined as institutional interfaces through which the effects of capital concentration and long-term systemic stabilization are realized.

Similarly, the concept of Highly Diffused Dynastic Wealth is used as an analytical category describing regimes of intergenerational capital retention and long-term strategic cognition rather than as a strictly operationalizable empirical unit.

The proposed model inevitably contains elements of structural simplification. Real elites, institutional frameworks, and dynastic structures are subject to:

| Pathology | Description |

|---|---|

| Internal Conflicts | Erosion of unity of purpose within dominant groups. |

| Coordination Failures | Disruptions in signal transmission between institutional layers. |

| Mechanism Degradation | Loss of functionality in core governance instruments. |

| Complexity Overflow | Exceeding the cognitive processing capacity of the system itself. |

Consequently, Static Capital should not be interpreted as a stable or indestructible structure. Historical experience demonstrates that dynasties disappear, institutions deteriorate, and long-term capital-retention regimes are vulnerable to entropy and endogenous forms of collapse.

Taking these limitations into account, the strategy of Old Thinking is understood not as a centralized governing subject but as a recurring historical pattern aimed at preserving long-term horizons and minimizing existential risk. Reality, in this sense, is not a system of governance but rather a field of competing cognitive regimes, institutional structures, and temporal horizons, whose interaction generates the institutional inertia of the capitalist system.

1.3. Epistemological Framework

Contemporary economic and political theory primarily operates at the level of Event-based cognition:

- Left-wing approaches — through the concept of exploitation;

- Liberal approaches — through the concept of efficiency;

- Institutional approaches — through the concept of coordination.

However, all of these remain at the level of observable effects and do not proceed to an analysis of the cognitive-temporal structure of order itself. A more fundamental level is associated with:

| Variable | Description |

|---|---|

| Temporal Horizons | The distribution of planning cycles between short-term and intergenerational layers. |

| Processing of Uncertainty | The asymmetry of cognitive strategies when confronting systemic shocks. |

| Risk Transfer | Mechanisms for transmitting costs between protected and vulnerable layers of the system. |

It is precisely this level that explains why stability emerges not despite conflicts, but through their structured redistribution.

1.4. Methodological Foundation

A significant portion of the mechanisms described in this paper is reconstructed through OSINT-based analysis:

| Source | Function |

|---|---|

| Public Registries | Identification of ownership titles and legal status. |

| Corporate Structures | Mapping ownership through subsidiaries and affiliated entities. |

| Legal Constructions | Analysis of trust agreements and nominee holding arrangements. |

| Biographical Trajectories | Examination of the relationship between an actor's career path and capital flows. |

| Macroeconomic Databases | Assessment of the impact of assets on overall market and debt dynamics. |

Accordingly, the model does not rely upon a single closed theoretical source but is assembled as a synthetic reconstruction of a distributed empirical environment.

1.5. Notes on the Paper

This text is not a scientific article in the strict sense of the term. Rather, it belongs to the domain of philosophical-systemic modeling incorporating elements of speculative capital theory and cognitive economics.

The works employed throughout the paper (Old and Young Thinking and Investor and Entrepreneur Cognition) serve as conceptual frameworks rather than completed empirical theories.

The initial hypothesis concerning the dominance of "Young Thinking" is treated as an analytical construct rather than a proven statement.

The persistence and resilience of the system, by contrast, point toward the existence of a deeper level of cognitive organization that may be described through the category of Non-Event Capital—a form of capital that does not manifest itself within the event-driven logic of markets and media.

1.6. The Philosophical Problem of Institutionalization

The central problem of contemporary philosophy of history lies in the tension between two forms of reductionism:

| Model | Description |

|---|---|

| Conspiratorial | Hyper-personalization of governance: emphasis on the exceptional role of specific actors, groups, and their direct will as the driving force of historical processes. |

| Institutional | Elimination of the subject: emphasis on the inertia of structures, coordination algorithms, and the rules of the game, where the individual merely performs a prescribed function. |

Pure institutionalism replaces the question of the subject with a system of rules while failing to explain the origin of their persistence and stability.

Within the proposed model, this "institutional gravity" is conceptualized through:

| Layer | Description |

|---|---|

| Non-Event Capital | The foundational layer: assets resistant to market shocks and event-driven noise. |

| Institutional Framework Capital | The implementation layer: a system of rules, trusts, and procedures that ensures the stability of ownership. |

| The Institutional Veil | The external layer: a "veil" that conceals the actual mechanisms of control from public observation. |

These categories describe the architecture through which strategic duration is maintained without the need to introduce a centralized governing subject.

1.7. Final Result (Meta-Level)

Thus, in the framework of this study, capital is understood as a cognitive-temporal structure rather than an economic variable.

Power is understood as a function of retaining duration.

And the stability of a system is interpreted as the result of asymmetries between cognitive regimes rather than as a consequence of centralized control or purely institutional self-regulation.

2. Institutional Thinking: The Economics of the Inflation Tax and the Reconfiguration of Macro-Risk

To demonstrate how the conflict between two cognitive regimes manifests itself at the macroeconomic level, let us examine the structure of capital distribution within the contemporary capitalist system using the United States as an example.

We begin with a statistical fact frequently cited in public discourse: approximately 1% of American households own around 50% of all stock market assets, while the top 10% own more than 90%.

This concentration is empirically confirmed by data from the U.S. Federal Reserve, including the Distributional Financial Accounts (DFA) and the Survey of Consumer Finances (SCF).

| Group | Share of Ownership |

|---|---|

| Top 1% | Control 50–54% of corporate equity capital. Instruments: direct ownership, trusts, and institutional structures (The Institutional Veil). |

| Top 10% | Control 88–92% of the stock market in aggregate. |

| Remaining 90% | Control only 8–12%, primarily through passive retirement vehicles such as 401(k) plans. |

These estimates are also supported by research conducted by major investment banks. Goldman Sachs Research, for example, notes: “The top 1 percent in net worth owns approximately 50 percent of all stocks held by U.S. households.”

Academic literature, including the work of Emmanuel Saez and Gabriel Zucman (University of California, Berkeley; NBER; Quarterly Journal of Economics), demonstrates that the concentration of financial assets at the top of the wealth distribution has returned to levels comparable to those observed prior to the 1929 crisis.

Within a purely institutional framework, these data are interpreted as evidence of static distributive inequality. However, when viewed through the lens of Old and Young Thinking and the Investor–Entrepreneur Cognition model, a different level of analysis emerges: the cognitive structure of risk redistribution.

In this interpretation, the upper layer of the system constructs a low-volatility strategic architecture within which risk does not disappear but is redistributed downward through institutional and financial channels, reinforcing the asymmetry of temporal horizons between different cognitive regimes.

2.1. The Mechanics of Risk Reconfiguration

Institutional capital does not eliminate risk as such; it changes its configuration and its recipient. The process of monetary intervention during market crises illustrates this cognitive principle in action.

| Stage | Description |

|---|---|

| Initial Risk (Top 1%) | Deflationary shock and liquidity crisis. |

| Systemic Effect | Loss of “systemic visibility” and degradation of the institutional memory embedded in capital. |

| Operational Response | Activation of Quantitative Easing (QE) and maintenance of ultra-low interest rates to stimulate currency depreciation. |

| Systemic Outcome | The risk of asset-price decline is shifted onto the consumer economy in the form of a distributed inflation tax. Risk migrates from the top 1% toward the remaining 90% of the population. |

2.2. The Asymmetry of Cognitive Regimes

At this point, a fundamental conflict emerges between two modes of processing reality described by the abstract model of the cognitive divide between Old Thinking and Young Thinking. Their differences are not merely economic but epistemological.

| Parameter | 90% of Population (Event-Based Cognition) | 1% of Population (Distribution-Based Cognition) |

|---|---|---|

| Perception of Inflation | A local catastrophe: “prices are rising, I am becoming poorer.” Reaction to discrete shocks. | A stabilization instrument: dilution of the real debt burden and support for corporate balance sheets. |

| Unit of Analysis | Operational budgets and a short-term “firefighting” horizon. | Capitalization and system survival in historical time (decades). |

| Protective Mechanism | Attempts to save more or index income (reactive resistance). | Influence through monetary architecture: asset values consistently outpace consumer inflation. |

2.3. Institutional Absorption of Risk Through Monetary Matrices

The statistical distribution of stock market ownership is not merely a passive snapshot of wealth. Rather, it constitutes the dynamic basis for the following theoretical proposition.

Proposition. Institutional risk absorption at the macroeconomic level utilizes monetary and inflationary mechanisms to convert structural asset volatility into distributed systemic costs. In doing so, it preserves the stability of long-term capital architectures at the expense of economic actors operating with shorter planning horizons.

This argument demonstrates that a low-risk condition for the strategic investor inevitably becomes a high-cost condition for the macro-system as a whole when the latter lacks sovereign mechanisms of protection.

What is commonly interpreted within everyday consciousness or superficial economic commentary as a “Federal Reserve mistake,” a “regulatory failure,” or simply “bad economics,” appears from the perspective of the institutional investor as a deliberate and carefully calculated low-risk architecture designed to preserve systemic longevity and dominance (success metric: longevity and dominance).

2.4. Systemic Outcome

Consequently, the fundamental mechanisms of macroeconomic stabilization—including the normative establishment of inflation targets—effectively protect the long-term substrate of Non-Event Capital.

This manifests itself as a process of transferring systemic costs onto short-term consumer cycles.

Within this framework, lobbying for monetary protection of the stock market ceases to appear as an abstract form of “political struggle” and instead reveals its immediate functional character: a technologically calibrated defense of the core assets of the top 1%, financed through a hidden inflation tax borne by the remaining 90% of the population.

3. Institutional Thinking: Cognitive Layers and the Fractal Distribution of Capital

To explicate the scale of cognitive asymmetry, it is necessary to translate percentage-based capital distributions into a demographically observable form. According to data from the U.S. Census Bureau and the Federal Reserve’s distributional datasets (SCF, DFA), the United States contains approximately 131–133 million households.

Projecting the structure of stock-market ownership onto this demographic foundation allows us to reconstruct not merely the economic, but also the cognitive-hierarchical architecture of the system.

- Top 1% (~1.3 million households): Controls more than 50% of all equity capital (either directly or through the Institutional Veil: funds, trusts, insurance vehicles, and pension structures).

- Top 10% (~13 million households): Controls more than 88–92% of the stock market in aggregate.

- Remaining ~90% (118–120 million households): Possess only residual access to the market through retirement vehicles (401(k)s, mutual funds), without operational control over capital allocation.

This structure demonstrates a fundamental principle: capital is not distributed evenly but is hierarchically organized through cognitive segregation.

3.1. The Macroeconomic Buffer: The Inflation Tax and the Regime of Event-Based Survival

The remaining segment of the macro-system, comprising approximately 90% of the population, consists of 118–120 million households. For this group, the stock market lacks operational agency. It exists either as an external informational abstraction or as an alienated retirement account (401(k)) that remains inaccessible until old age.

Their economic reality is entirely determined by the regime of Event-Based Cognition, which operates within the boundaries of a short-term operational budget defined by housing costs, debt obligations, food prices, and fuel expenses.

When the regulator (the Federal Reserve) engages in monetary intervention to absorb systemic risks for the benefit of approximately 1.3 million households—thereby preventing the nominal degradation of capital and the collapse of institutional architecture—the costs of that stabilization, in the form of an inflation tax on consumption, are effectively transferred onto 120 million households.

At the level of the macro-structure, this process functions as a classical protective circuit: the vast peripheral mass (90% of the system) is transformed into a Cognitive Buffer Zone.

This buffer zone serves as a shock absorber, absorbing macroeconomic disturbances in order to preserve the stability, coherence, and continuity of the systemic core (the top 1%).

3.2. Fractal Cognitive Layering Within the Dominant Class

An examination of the internal structure of the top 1% (approximately 1.3 million households) reveals a phenomenon of fractal inequality: at every new level of magnification, ultra-wealthy groups dominate merely wealthy groups according to the same matrix through which the top 1% dominates the rest of society.

Within this stratum, three cognitive-economic layers can be distinguished, each defining a distinct mode of operating concentrated capital.

| Layer | Functional Role | Cognitive Regime |

|---|---|---|

| Top 0.1% – 0.01% | Core: Distribution Managers | Non-Event Capital / Absolute Old Thinking |

| Top 0.5% | Institutional Glue: Corporate Class | Stock-Based Compensation / Hybrid Cognitive Vision |

| Lower Segment of the Top 1% | Rentiers and Highly Paid Professionals | Passive Investors / Psychologically Young Thinking |

3.2.1. The Core of the System: The Top 0.1% and Top 0.01% (Distribution Managers)

This layer occupies the apex of the hierarchy and consists of approximately 13,000 to 130,000 families.

Profile. Founders of transnational technological and industrial conglomerates, hereditary dynasties, holders of controlling equity stakes, and ultimate beneficiaries of the largest alternative investment funds (Private Equity and Hedge Funds).

Ontology of Capital. Their capital substrate lies outside the category of “liquid money held in bank accounts.” It is pure structural capital: voting shares, controlling stakes in critical infrastructure, prime real estate, and institutions of systemic influence.

Cognitive Regime. This layer represents the purest embodiment of Old Thinking. Ownership of the stock market here is not synonymous with passive dividend extraction; rather, it is equivalent to designing, shaping, and preserving the rules of the game itself.

Possessing the highest concentration of lobbying capacity, this group tends to perceive monetary inflation targeting at levels of 3–4 percent (instead of a harsh, cleansing deflationary adjustment) as a technological instrument for preserving the nominal valuation of multi-billion-dollar asset portfolios.

3.2.2. The “Institutional Glue” Layer: The Top 0.5% (The Upper Corporate Class)

This stratum encompasses approximately 400,000–500,000 households.

Profile. C-level executives (CEOs, CFOs, COOs) of S&P 500 companies, senior partners in leading investment, legal, and consulting firms (Wall Street and the Magic Circle), as well as serial entrepreneurs.

Ontology of Capital. The wealth of this layer is primarily generated through long-term stock-based compensation programs and stock options.

Cognitive Regime. This group serves as a transitional bridge between operational and distributional thinking. While managing the day-to-day functioning of complex systems, they remain personally dependent on capitalization trajectories and market valuations. Their cognitive apparatus is tightly synchronized with the imperative of sustaining market growth at virtually any cost, since a market devaluation would render their stock options worthless.

This represents a functional form of Old Thinking. However, its limitation lies in the absence of the holistic metasystemic vision possessed by the architects of the rules themselves—the actors described in Section 3.2.1.

3.2.3. The “Upper Layer of Salaried Labor”: The Lower Segment of the Top 1% (Rentiers and Professionals)

The remaining segment consists of approximately 700,000–800,000 households.

Profile. Extremely high-income specialists: leading surgeons, corporate attorneys, senior-grade IT architects, investment advisors, and regional real-estate developers.

Ontology of Capital. Their wealth is predominantly passive and cumulative in nature. Capital accumulated through intellectual rent or local business activity is subsequently reinvested into index funds (ETFs), mutual funds, or retirement vehicles.

Cognitive Regime. Epistemologically, they remain within the framework of Young Thinking, since their primary income remains linearly tied either to the value of their personal time or to the success of discrete transactions.

Financially, however, they have already been incorporated into the long-term architecture of capital. Although they are not the creators of Wall Street’s rules, they function as the system’s principal fellow travelers. For this group, a market crash represents a personal catastrophe—the destruction of strategies aimed at achieving financial independence and early retirement (the FIRE movement).

3.3. The Architecture of Lobbying: The Political Shield and the Mechanisms of Existential Risk Offloading

In situations of macroeconomic shock, the substrate of the top 0.1% activates lobbying algorithms aimed at protecting the stock market through monetary expansion and controlled inflation.

In this process, the upper strata utilize the broader top 1% and top 10% as a living socio-political shield.

Within the public media sphere, such rescue operations are not presented as the protection of the multi-billion-dollar nominal valuations of the ultra-wealthy. Instead, they are framed through narratives such as “protecting middle-class retirement savings,” “preserving jobs,” or “ensuring the stability of retail investors.”

As a result, the classical historical phenomenon of currency debasement acquires a modern cognitive form. Approximately 120 million American households (the bottom 90%), locked within an event-based mode of cognition, pay a hidden inflation tax under the ideological banner of “saving the national economy.”

In practical terms, however, they contribute to the preservation of the scale and structure of capital concentrated within the upper 130,000 households.

3.4. Systemic Outcome

This pattern demonstrates the invariance of a cognitive strategy.

Historical analysis would likely reveal that 300, 500, 1,000, or even 5,000 years ago, a comparable cognitive regime—adapting itself to the technological and institutional conditions of its time, from coin debasement in the Roman Empire to the fiscal matrices of ancient Eastern despotisms—would have employed different operational solutions.

Yet the invariant and primary element remains the same: a deep existential strategic orientation toward the management of risk.

At its core lies the capacity of the system’s nucleus to engage in Existential Risk Offloading—the transformation of its own localized threats into distributed systemic costs borne by the periphery.

It is precisely this mechanism that most fully captures the ontological distinction between Old Thinking and Young Thinking.

4. Static Capital: Institutional Retention of Strategic Duration

The existing global capitalist system has been functioning for centuries. By its very nature, the institution of property implies not merely the formal registration of rights, but the long-term preservation of ownership. The logic of preservation requires a specific existential strategy.

In the basic theoretical model (Old and Young Thinking), this phenomenon is described at the level of a macro-narrative. However, within the formal structure of systems analysis, it must be identified as the Fundamental Institutional Layer, or Static Capital.

This non-public layer of capital is a critical element that ensures the dual-layered architecture of capitalism. Without the preservation of this static constant, capitalism would be incapable of reproducing itself across historical duration and would be exposed to entropic disintegration after several cycles of dominance by destructive forms of Young Thinking.

At the empirical level, the carriers of this cognitive matrix are the so-called Old Money groups: transnational dynastic pools of wealth, historical aristocracies, and established industrial families. These actors are compelled to think several strategic cycles further ahead than conventional investment managers or public institutional funds.

Within the framework of the proposed theory, organizations such as BlackRock, Vanguard, and State Street appear not as ultimate beneficiaries, but as higher-level operators. They function as technological interfaces of the low-risk strategy characteristic of Old Thinking, managing allocations within the public sphere, while Static Capital remains the true, invisible author of the architecture of existing existential duration.

4.1. The Dual-Circuit Nature of Capitalist Duration

The structure of the system can be divided into two fundamental circuits:

| Category | Description |

|---|---|

| Dynamic Capital | Operational Layer: Funds, corporations, public markets, and highly liquid assets. |

| Static Capital | Cognitive-Institutional Layer: Dynasties, private trusts, family structures, and intergenerational retention of control. |

Static Capital does not engage in direct market competition with public institutions of capital management. Instead, it occupies the position of their primary beneficiary and client.

When macroeconomic statistics indicate that BlackRock manages approximately $10–11 trillion in assets, systems analysis requires a distinction between the operator and the owner. These trillions do not belong to the corporation itself; rather, they represent consolidated pools of investors' capital.

A significant share of these resources is accumulated through closed Family Offices, Blind Trusts, and Private Foundations registered in jurisdictions characterized by exceptionally high levels of confidentiality and asset protection (Luxembourg, Liechtenstein, the Cayman Islands, and the U.S. states of South Dakota and Delaware).

The actual chain of ownership and distribution of cognitive regimes forms the following hierarchical structure:

National Wealth / S&P 500 Equity Holdings

Public Facade of the System

▲

Public Giants (BlackRock, Vanguard, State Street)

Interface: Transparency and Public Visibility

▲

Institutional Trusts / Blind Pools

Intermediate Layer: Anonymity and Protection

▲

Old Capital (Families / Dynasties)

Core Layer: Old Thinking

4.2. The Functional Logic of Static Capital: Retention Rather Than Income

The fundamental mistake of classical economic analysis is the interpretation of capital as a stream of returns.

Capital is:

- not income;

- not profit;

- not an asset.

Within the logic of Static Capital, capital is:

▸ A mechanism for retaining structural control across time.

Planning horizon:

| Type of Capital | Planning Horizon |

|---|---|

| Standard Capital | 10–30 years |

| Static Capital (Intergenerational Circuit) | 100–300 years |

4.3. The Cognitive Regime of Static Capital: Absolute Historical Horizon, Anonymity, and Risk Outsourcing

While a conventional institutional investor typically operates within a multi-decade horizon, Static Capital unfolds its strategies within the framework of intergenerational time, ranging from 100 to 300 years.

The objective of this cognitive model is not the extraction of short-term speculative profits or the achievement of annual stock appreciation by a certain percentage. Rather, it is directed toward maintaining comprehensive control over the physical, infrastructural, and financial fabric of the historical world. Within this framework, first-tier institutional funds perform two fundamental functions for the core:

Institutional Opacity.

Intermediary funds make it possible to hold strategic sectors—including energy systems, land portfolios, and transportation infrastructure—without generating significant social or political resistance. In legal documentation, ownership of an infrastructure asset is attributed to an impersonal index fund rather than to a specific heir of a nineteenth-century financial dynasty. This arrangement enables the older cognitive matrix to expand and preserve its sphere of influence without direct public visibility.

Operational Risk Outsourcing.

Old Capital delegates the technical routine of implementing its existential objectives to automated risk-analysis systems (such as BlackRock’s Aladdin platform). This enables the core to remain a low-risk participant while retaining a diversified share of global economic output. Consequently, risk becomes a technical function rather than an existential threat to the owner of capital.

4.4. The Phenomenon of Institutional Static Capital

This model of Static Capital is not intended as a conspiratorial narrative. Rather, it represents a deductive theoretical derivation of a fundamental institutional layer whose existence is functionally necessary for maintaining the strategic stability of the system.

Within classical institutional economics, similar phenomena are typically described through established academic concepts associated with institutions as formal and informal constraints, transaction costs, path dependence, and the evolution of rules and organizations. In the present work, however, a more generalizing category—Static Capital—is employed.

Institutional opacity and intergenerational capital protection constitute foundational elements of a low-risk long-term architecture. This architecture is based upon a strict structural separation between beneficial ownership and operational management.

Large asset-management organizations form an intermediate cognitive layer behind which a non-public layer of family wealth remains concealed. This arrangement creates a system of dual protection:

- Political and Regulatory Shield: Long-term capital is insulated from electoral, fiscal, and political disruptions through the legal anonymity provided by institutional mechanisms.

- Temporal Distribution of Risk: Cognitive functions are organized on a multi-generational scale. Ultimate beneficiaries remain largely invisible to both regulatory and public scrutiny while transferring operational risks and public pressure to intermediary management structures.

4.5. The Disproportion Between Public Capital and Static Capital: Those Who Do Not Appear in Rankings

The contemporary financial architecture generates a fundamental cognitive paradox: the individual wealth of technological leaders (for example, Elon Musk) represents “young,” open, and publicly visible money, whereas the aggregate volume of Static Capital constitutes “old” institutional money. Institutional capital, viewed as a consolidated collective formation, qualitatively exceeds any individual featured in Forbes or Bloomberg rankings in terms of resilience, scale, and depth of control over foundational assets.

The absence of this layer from public wealth rankings is largely a consequence of the algorithms by which such rankings are constructed. Wealth rankings employ a linear metric: they multiply the number of shares in a public company by their current market value and assign the result to a specific individual. A figure such as Elon Musk possesses a verifiable ownership stake in Tesla and SpaceX. His wealth therefore represents a classic form of capital oriented toward events and venture growth (Event-based / Venture-backed), fluctuating alongside market conditions, media narratives, and quarterly reporting cycles.

Static Capital is structured according to an entirely different matrix. A consolidated dynastic pool hypothetically amounting to $500 billion is never assigned to a single individual. Instead, it undergoes fractal dispersion.

| Strategy | Description |

|---|---|

| Familial Diversification | Capital is dispersed throughout an extended family tree (for example, across 300 or more members). Effect: removal from the focus of global monitoring systems and media wealth rankings. |

| Blind Trusts | Assets are deposited into isolated structures located within confidentiality-oriented jurisdictions (such as Liechtenstein or Delaware). Effect: separation of the direct connection between beneficiary and asset. |

| Private Foundations | Capital is transferred into the legal form of philanthropic institutions. Effect: de jure loss of personal ownership while preserving de facto control through a family-controlled governing board. |

This architecture allows substantial concentrations of wealth to persist across generations while remaining largely invisible within methodologies designed to measure individual net worth. From the perspective of public rankings, such capital appears fragmented, legally detached, or institutionally transformed. From the perspective of long-term strategic continuity, however, it may continue to function as a coherent mechanism for preserving control across extended historical horizons.

4.6. The Ontological Difference in the Nature of Capital: Virtual Valuation and Physical Substrate

The capital of the leaders of Young Thinking is, to a significant extent, virtual in nature—it represents the capitalization of market expectations regarding future products, technologies, and growth trajectories. In the event of a large-scale market collapse of 70 percent, the “paper” wealth of nominal billionaires declines proportionally. The cognitive regime of such actors is oriented toward aggressive expansion, the creation of new markets, and the acceptance of radical entrepreneurial risk. This strategy is capable of both “discovering America” and precipitating rapid systemic collapse.

By contrast, Static Capital, through intermediary institutional structures, maintains control over the foundational physical infrastructure of human civilization:

| Category | Assets |

|---|---|

| Natural Resource Layer | Strategically significant agricultural land and major global aquifer systems. |

| Infrastructure Layer | Mainline railways, deep-water ports, and energy distribution networks. |

| Urban Layer | High-value commercial real estate located in the historic centers of global capitals. |

| Financial Layer | Sovereign debt instruments and government bonds issued by major states. |

These assets are generally not exposed to the risk of complete nominal disappearance. During periods of deep systemic crisis, when actors operating within the Young Thinking paradigm lose billions through equity devaluation, this foundational layer—utilizing the mechanisms of institutional funds under its influence (BlackRock, Vanguard, and other major asset-management structures)—acquires the opportunity to engage in large-scale purchases of depreciated real assets.

It is precisely here that the operational logic of a low-risk strategic architecture becomes visible.

4.7. Cognitive Advantage: “Key-Man Risk”

Within the venture capital and technology entrepreneurship ecosystem, one of the principal vulnerabilities is Key-Man Risk. The removal, incapacitation, or degradation of a central leader (for example, Elon Musk) can immediately undermine the valuation of associated organizations, because the stability of the business is closely tied to a personal brand and an individual cognitive apparatus.

Static Capital has effectively eliminated this vulnerability. Within the structure of old capital there is no “key individual”; governance is deeply depersonalized and algorithmized.

If a particular heir within a dynastic structure demonstrates managerial incompetence, the mechanisms of the family office can remove that individual from the strategic decision-making process without institutional conflict. The individual is transferred to a fixed rentier income arrangement, while control over the assets is delegated to professional institutional managers.

Capital thereby begins to function as an autonomous algorithm capable of reproducing itself across historical time.

This layer does not compete with public business leaders in Forbes rankings. From the perspective of Static Capital, competition with actors who effectively service the technological and financial macrostructure upon which it relies possesses little strategic significance.

While the entrepreneur builds factories, launches new ventures, and assumes extraordinary operational risks, the subjects of Non-Event Capital maintain control over the indices, financial infrastructures, and institutional frameworks into which those factories and enterprises will ultimately be integrated once the industry reaches maturity.

In this sense, the distinction between Young Thinking and Non-Event Capital is not primarily a distinction of wealth, but a distinction of temporal position within the architecture of civilization itself: one layer creates and disrupts, while the other absorbs, stabilizes, and preserves.

5. Static Capital: An Empirical Reconstruction of the Structure of Systemic Wealth

To explicate the operational scale of Institutional Framework Capital and to reconstruct in detail the empirical foundation from which the parameters of Static Capital are derived, it is necessary to completely exclude media-driven and populist rankings such as Forbes or the Bloomberg Billionaires Index from the methodological framework.

The real macroeconomic statistics of Static Capital are not assembled from press publications but through comprehensive structural analysis of the closed infrastructure of wealth management—multi-family and single-family offices, trust registries, and internal reports produced by the largest first-tier investment banks.

Presented below are consolidated OSINT calculations, methodologies, and verified data sources that reflect the architecture of Static Capital distribution.

5.1. Levels of Static Capital

If we examine Static Capital—which, in terms of financial resilience, intergenerational survivability, and aggregate net asset volume, qualitatively surpasses the volatile capital of technological leaders (whose fortunes are exposed to market fluctuations within a range of $200–300 billion)—this structure can be clearly differentiated into two strategic levels:

Level 1: The “Global Core”

- Scale: 2,500–3,000 sovereign and dynastic family clusters.

- Control: More than $15–20 trillion (assets exceeding $1 billion).

- Essence: Capital is fractally distributed through trust structures, making the identification of a single center of control impossible.

- Examples: European and American dynasties, monarchical wealth pools, and Asian conglomerate families.

Level 2: The “Institutional Foundation”

- Scale: Approximately 50,000 family clans (around 190,000 UHNWI individuals).

- Control: More than $24–30 trillion (assets exceeding $30 million).

- Essence: The foundational layer supporting private investment structures that maintain influence over critical infrastructure, land, and sovereign debt instruments.

5.2. Data Sources and the Methodology of Comprehensive Audit

Because the capital under examination is protected by The Institutional Veil, its verification requires the synthesis and cross-analysis of data originating from three independent sectors of the asset-management industry.

A. Family Office Databases and Advisory Analytics

Single-Family Offices are created specifically to serve the interests of particular dynasties. Their balance sheets remain inaccessible to public regulatory scrutiny, yet their transactional activity is monitored by specialized intelligence agencies.

PwC Global Family Office Deals Study

PwC’s comprehensive audit verifies the existence of more than 20,000 family offices worldwide (approximately 7,160 located in the United States and 2,720 in Singapore). According to PwC data, more than 50 percent of the structures that partially disclose operational metrics manage at least $2.5 billion each.

FINTRX & Altrata (Predictive Intelligence)

These predictive-analytics platforms monitor between 8,000 and 9,000 major Single-Family Offices. The fifty largest institutional family offices—including Walton Enterprises, the Wertheimer family’s Mousse Partners, Waycrosse, and others—collectively control approximately $2.4 trillion, a figure comparable to the annual GDP of major European economies.

B. Global Wealth Reports and Macrosociological Studies

Altrata (World Ultra Wealth Report / Investable Assets Model)

This represents one of the principal sources of structural data concerning the distribution of ultra-high-net-worth capital. Within the applied model of investable asset distribution, the ultra-wealthy segment ($30 million+) accounts for only 1.1–1.2 percent of all global millionaires while controlling 32.4 percent of total private wealth worldwide ($59.8 trillion).

Knight Frank Wealth Sizing Model

This research framework estimates the density and distribution of concealed wealth through algorithms that evaluate prime real estate holdings, private merger-and-acquisition transactions, and ownership stakes in private equity funds.

C. Internal Deposited Research from Investment Banks (UBS, Citibank, BlackRock)

These institutions function as direct custodians, clearing centers, and brokerage intermediaries for the hidden layer of wealth.

BlackRock Global Family Office Report & Citi Private Bank Survey

Surveys covering hundreds of family offices—with average assets ranging from $1.8 to $2.1 billion per structure—reveal the direction of Strategic Asset Reallocation within physical capital portfolios.

For this layer, priority is assigned to alternative private assets, representing up to 45 percent of aggregate portfolios:

- Private Debt

- Large-scale infrastructure projects

- Data-center networks

- High-productivity agricultural land

5.3. Comparative Analysis: A Heuristic Matrix of Capital Cognitive Regimes

| Parameter | “Paper” Capital (Young Thinking) | “Physical” Layer (Old Thinking) |

|---|---|---|

| Verification Source | Stock-market quotations (SEC, Bloomberg) | Closed Family Office registries (PwC, FINTRX, Altrata) |

| Point of Identification | Specific individual or brand (Tesla, SpaceX) | Network structure of trusts and nominee arrangements |

| Scale and Dynamics | Approximately $200–300 billion (high volatility) | More than $15–20 trillion (resilience to shocks) |

| Asset Substrate | Technology equities (venture risk) | Land, infrastructure, gold, private equity |

5.4. Systemic Conclusion

Consequently, the empirical aggregate of Non-Event Capital is derived not from media rankings of individual wealth but from the structural and functional analysis of the institutions that manage such capital.

This foundational layer does not operate as a monolithic conspiracy. Rather, it functions as a geographically dispersed, legally protected, and institutionally shielded network of family offices and trust structures.

The aggregate economic gravity and depth of cognitive control embodied within this network exceed by multiple orders the potential influence of any individual public actor. This observation supports the central thesis that the stability of capitalist space is maintained through the largely invisible transfer of systemic risks toward the peripheral layers of the macroeconomic structure.

6. Manifestations of Historical Flashpoints

Within political history there exists a unique type of actor — “architects of systemic compromise” or “deep technocrats.” Such figures emerge on the political stage at moments when classical public politics (democratic institutions, electoral noise, and ideological confrontation) reaches a state of total strategic deadlock.

Three characteristic features can be identified for such actors:

- Institutional Embeddedness: a presumed connection to The Establishment Capital or supranational structures, granting them immunity from immediate electoral anxieties and short-term political pressures.

- Fundamental Cognitive Superiority: an interdisciplinary synthesis in which economics, risk management, and statecraft are fused into a unified framework as a result of both exceptional strategic reasoning and a specific process of self-education aimed at achieving holistic thinking rather than fragmented understanding of sector-specific phenomena.

- Strategic Agency and Capacity for Institutional Mediation: expressed through the ability to translate conflicting political regimes into a language of procedures, compromises, and long-term solutions. This reduces the amplitude of ideological confrontation and compels opponents to shift from a propagandistic register toward a pragmatic one. Such a capacity constitutes an element of a distinctive cognitive and institutional position that is rarely captured by classical institutional theories, yet rests upon durable structures of social order and provides a high degree of internal coherence for actors operating within this particular framework.

Let us focus on several illustrative figures.

6.1. Jean Monnet — The Transition from Geopolitics to Institutional Design

Jean Monnet represents an early form of such an operator under conditions created by the collapse of the European balance following the World Wars.

Institutional Trajectory

His initial position emerged outside the framework of a conventional state career, within a transnational commercial environment (the Monnet & Co cognac business), where the primary unit of analysis was resource flows rather than national borders.

Systemic Logic of Action

During the World Wars, he worked on logistics and the coordination of Allied supplies, confronting the practical necessity of managing large-scale distributed systems under catastrophic conditions.

Institutional Reconfiguration of Europe

In the postwar period, he proposed a model in which the critical resources of military power (coal and steel) were removed from exclusive national sovereign control and transferred into a supranational governance framework through the European Coal and Steel Community (ECSC).

Systemic Interpretation

Monnet implemented a shift from the geopolitical logic of conflict toward the logic of institutional separation and shared management of strategic resources, effectively transforming war as a form of competition into a regime of structural regulation.

6.2. Valéry Giscard d’Estaing — The Institutionalization of European Coordination

Giscard d’Estaing represents a phase in which institutional forms of coordination became a stable component of the European system.

Institutional Context

He emerged from the highest administrative, political, and industrial-bourgeois circles of France, embedded within a long tradition of state governance.

Cognitive Framework

His education within elite engineering and administrative institutions cultivated an ability to think in terms of systemic stabilization rather than localized political struggle.

Institutional Outcomes

He participated in the creation of the European Monetary System, which became an intermediate architecture between national currencies and future monetary integration.

Systemic Interpretation

The role of this figure consisted in translating a nationally fragmented system into a regime of coordinated monetary and financial interaction.

6.3. Paul Volcker — Stabilization Through Systemic Compression

Paul Volcker represents a model of restoring macroeconomic stability through the radical suppression of inflationary expectations.

Systemic Context

The stagflation crisis of the late 1970s constituted a rupture between monetary policy and real economic dynamics.

Institutional Solution

A sharp increase in interest rates to levels capable of producing a deep recession while simultaneously restoring confidence in the monetary system.

Regime of Stability

Despite intense political and social pressure, the chosen course was maintained until inflationary expectations were stabilized.

Systemic Interpretation

The objective was not the optimization of current economic growth but the restoration of the fundamental monetary framework as a prerequisite for the long-term stability of the system.

6.4. Comparative Structure of Stabilization Operators

| Figure | Institutional Position | Type of Systemic Action | Macroeconomic Effect |

|---|---|---|---|

| Jean Monnet | Transnational economic networks | Transformation of conflict into supranational resource governance | Institutional integration of Europe |

| Valéry Giscard d’Estaing | State-industrial elite | Monetary and financial coordination | Stabilization of the European economic architecture |

| Paul Volcker | Monetary institutional system | RIGOROUS SUPPRESSION OF INFLATIONARY EXPECTATIONS | Restoration of monetary-system resilience |

6.5. Systemic Conclusion

Figures of this type do not emerge as expressions of a “hidden center of control.” Rather, they arise as the result of a temporary concentration of the institutional and cognitive capacities required for systemic self-stabilization.

Their function is to restore the fundamental parameters of duration and predictability during periods of crisis, thereby enabling the system to return to a mode of reproduction and continuity.

Within the terms of the broader model, they function as temporary nodes for the restoration of the strategic horizon, facilitating the transition from crisis-induced fragmentation toward a renewed architecture of coordination.

The phenomenon of “deep technocrats” demonstrates that during moments of extreme macro-systemic imbalance, the sphere of The Establishment Capital may sacrifice immediate conjunctural interests in order to preserve the broader framework of strategic continuity. By elevating figures possessing strong existential autonomy, the system temporarily enters a mode of direct cognitive governance. In such periods, the center of decision-making partially shifts away from electoral logic and toward the logic of institutional resilience.

7. Non-Event Capital: British Institutional Infrastructure as a Mechanism for Preserving Strategic Duration

Let us assume that the continental European elite maintains equilibrium through its linkage with historical institutions and the Euro-bureaucratic apparatus; in this sense, British Highly Diffused Dynastic Wealth has brought this mechanism to an absolute, exemplary perfection.

They do not merely utilize the depersonalization mechanisms of Old Thinking — this tradition, within the context of more than a thousand years of history, has created a global legal and financial operating system into which the capital of all other players settles, including American venture capitalists and Asian billionaires.

If we very conditionally reconstruct the structure of British Highly Diffused Dynastic Wealth through a three-layer model that is easier to conceptualize — the Institutional Veil, Cognitive Sovereignty, and the Concrete Avatar — it would appear as follows:

BRITISH NON-EVENT CAPITAL

│

STRUCTURAL LAYER

Institutional Veil

• The quasi-state of the City

• Discretionary Trusts

• Land (Non-Event Capital)

COGNITIVE LAYER

Cognitive Sovereignty

• Permanent Secretaries

• The Eton / Oxbridge (PPE) filter

CONCRETE AVATAR

Systemic Subject

• Mark Carney

• Horizon Management

7.1. Structural Layer: The Empire of Offshore Trusts and the City

The British elite is unique in that it survived the dismantling of the actual British Empire without losing control over global financial flows. It executed a remarkable cognitive maneuver: replacing physical territories (colonies) with legal jurisdiction.

This network functions as a three-layer filter that almost completely dissolves the notion of individual wealth:

- The City of London (the City) — a unique corporate jurisdiction within London, possessing its own governance system, institutions, and historically developed autonomy. This is the core where institutional capital is concentrated and packaged.

- The Crown Dependencies and Overseas Territories — the Cayman Islands, Bermuda, Jersey, Guernsey, and the British Virgin Islands. These are not merely “tax havens” for tax avoidance but a global infrastructure of trusts, foundations, and mechanisms for intergenerational capital preservation. Money transferred into a British Discretionary Trust legally ceases to belong to a specific individual. The trustee becomes the formal owner, while the economic benefits may remain within the same family for generations.

- The Land Monopoly (The Crown Estate and the Duchies) — while representatives of Young Thinking build corporations and increase market capitalization, the old British landed aristocracy maintains control over the most valuable districts of central London — Mayfair, Belgravia, and Chelsea. This land is not sold; it is leased for 99 or 999 years. Here land represents the ultimate form of Non-Event Capital: an asset capable of outliving governments, crises, currencies, and generations.

7.2. The Cognitive Layer: The Permanent Secretary

The British state apparatus is organized in such a way as to largely neutralize the risk of incompetence among public politicians. While ministers (Boris Johnson, Liz Truss, Rishi Sunak) change at kaleidoscopic speed, generating media noise, institutional memory and administrative continuity within ministries are largely ensured by Permanent Secretaries — effectively irremovable technocrats who serve for decades.

This layer is reproduced through a rigorous institutional selection filter:

Eton / Harrow → Oxbridge (PPE) → City of London / Foreign Office

(although, to a significant extent, this model represents an idealized scheme for reproducing the elite cognitive layer).

This is not a matter of a formal elite conspiracy, but rather a mechanism for reproducing a cognitive regime within which strategic thinking, uncertainty management, and the ability to maintain a long-term time horizon are transmitted through systems of education, social connections, and institutional selection.

They possess what may be termed Cross-domain Knowledge Integration — the ability to connect maritime law, ECB macroeconomic indices, rare-earth supply chains, and military risk management into a single long-term strategy.

7.3. The Avatar of the System: Mark Carney as an Operator of Horizons

If one attempts to identify a personalized interface of this institutional layer, it becomes visible, for example, in figures such as Mark Carney.

His trajectory is not a career trajectory but a structural one:

- Education: Harvard → PhD Oxford (the PPE environment as a cognitive incubator of elite formation).

- Private Capital: Goldman Sachs (global risk markets as a practical school of capital allocation).

- Institutional Authority: Bank of England (the first foreign Governor in the institution’s history).

- Global Superstructure: Financial Stability Board (G20), followed by Brookfield Asset Management (~$1 trillion in infrastructure and alternative assets).

Carney’s key conceptual contribution is the idea of the “Tragedy of Horizons”: the structural inability of public policy and markets to account for long-term systemic risks.

This formalizes a fundamental divide:

- politics lives through electoral cycles;

- markets live through quarterly reports;

- risk systems operate through multi-decade trajectories.

Carney operates precisely within the third regime.

Conceptual Conclusion

The British elite will never send a flamboyant public politician to a negotiation table, because the objective of the British diplomatic and financial apparatus is not to “win on television,” but to codify new rules of the game within international law and financial regulations.

If Monnet represents the ideal negotiator for preserving a geopolitical status quo, then figures such as Carney are the architects who, after those negotiations have concluded, rewrite the rules governing capital flows, sanctions regimes, and sovereign guarantees for the next half-century.

The British institutional model is neither a state nor a market in the classical sense. It is a cognitive-legal infrastructure that:

- separates capital from personal identity;

- translates governance into the regime of long-duration time horizons;

- depoliticizes resource allocation through legal form;

- stabilizes the global system through institutional inertia.

If continental models balance between politics and economics, the British model functions as the operating environment within which these distinctions have already been absorbed in advance.

This is why it appears not as a player within the global financial system, but as one of its architectural layers.

8. Methodological Note

The present interpretation constitutes an analytical model and does not imply the existence of a single centralized subject coordinating the global distribution of capital. Empirical evidence regarding the high concentration of wealth is supported by research on capital and wealth distribution, including materials produced by the OECD, UBS, and academic studies in the field of wealth distribution.

At the same time, the concepts of Static Capital and the related categories employed in this work represent theoretical abstractions intended to describe a set of heterogeneous mechanisms of intergenerational asset preservation rather than empirically identifiable entities. In reality, the phenomenon involves a multitude of autonomous and institutionally heterogeneous actors — families, foundations, trusts, family offices, and asset-management structures — possessing different strategic interests and not constituting a single coordinated collective subject.

Additionally, the following methodological limitations of the model should be taken into account:

- A significant portion of data concerning private capital, trust structures, and wealth distribution is characterized by limited transparency and incomplete observability;

- Estimates of capital concentration and distribution are inherently approximate and depend substantially on the selected methodology of data aggregation and interpretation;

- By design, the model focuses on mechanisms of stability and strategic duration and therefore may systematically underestimate processes of internal fragmentation, conflict, and disintegration within elite and institutional structures;

- Institutional anonymity cannot be regarded as an indicator or proof of the existence of a hidden center of control;

- Statistical correlations between institutional structures do not constitute sufficient grounds for inferring coordination or the existence of a unified strategic design;

- The categories employed in this work (Static Capital, Non-Event Capital, Institutional Framework Capital) are original analytical constructs and do not belong to the standardized conceptual corpus of contemporary economic science;

- The proposed model does not claim to provide an exhaustive or uniquely correct explanation of the functioning of the capitalist system and should be understood as one possible theoretical framework for interpreting the relationships between capital, time, institutional stability, and the distribution of risk.

9. AI & Data Collection Disclosure

This research was conducted within the framework of a hybrid intelligence methodology, in which cognitive sovereignty, systemic interpretation, and final theoretical validation remain entirely the responsibility of the author. Generative language models (Large Language Models, LLMs) were employed exclusively as an instrumental layer of technical support, without delegating to them the functions of conceptual design, theoretical synthesis, or the formulation of final conclusions.

The use of AI was limited to operational tasks of data processing, structuring, and preliminary aggregation within the analytical architecture defined by the author.

9.1. Data Collection & OSINT Structuring

The empirical foundation of the study was assembled through targeted content analysis and OSINT-based aggregation of open institutional sources, including macroeconomic reports, analytical databases, and public institutional registries.

At the stage of primary processing, language models were used as instruments for:

- structuring heterogeneous information arrays;

- chronological normalization of data;

- thematic clustering of cases and institutional trajectories.

In particular, they were employed to systematize:

- biographical and institutional trajectories of architects of systemic compromise (Jean Monnet, Valéry Giscard d’Estaing, Paul Volcker, Mark Carney);

- institutional structures of capital management (The Crown Estate, discretionary trusts, family offices);

- macroeconomic and governance frameworks of asset allocation within Anglo-Saxon and Continental institutional systems.

All generated and aggregated data were subsequently subjected to independent cross-verification by the author using multiple external sources.

9.2. Textual Engineering & Formalization

Generative models were employed as instruments of textual engineering, including:

- unification of the syntactic structure of analytical sections;

- standardization of tables, diagrams, and enumerations according to a consistent academic-analytical format;

- technical optimization of the coherence of argumentative chains without altering their semantic content.

AI was not used as a source of conceptual claims or theoretical invariants within the research.

9.3. Authorial Intellectual Framework and Responsibility

All key theoretical constructs employed in the study, including:

- the Three-Layer Model of Subjectivity;

- the Old and Young Thinking dichotomy;

- the concept of Non-Event Capital;

- the Institutional Framework Capital model;

are the result of the author's independent development and systematization.

Generative tools did not participate in the formation of the underlying ontological assumptions of the research and were utilized exclusively at the level of auxiliary analytical processing.

9.4. Final Responsibility

The author retains full intellectual and methodological responsibility for the content, interpretations, and conclusions of this research, including its conceptual integrity and cognitive architecture.