Investor and Entrepreneur Cognition:

Risk Transformation and the Institutionalization of Capital — From Event-Based Uncertainty to Distribution-Based Risk Governance (Working Preprint)

A formal companion paper to the philosophical essay: Why Investors Think Differently Than Entrepreneurs: The Philosophy of Finance and the Cognitive Divide Between Young and Old Thinking

APA Citation / Zenodo Preprint:

Rusnak, A. (2026). Investor and entrepreneur cognition: Risk transformation and the institutionalization of capital — From event-based uncertainty to distribution-based risk governance (Working preprint). Zenodo. https://doi.org/10.5281/zenodo.20340488

Positioning Statement

The present paper is not an independent theoretical narrative.

It constitutes the formalization layer of a broader research program. The philosophical foundations of this research are developed in the essay: Rusnak A. (2026) Why Investors Think Differently Than Entrepreneurs: The Philosophy of Finance and the Cognitive Divide Between Young and Old Thinking. Zenodo. https://doi.org/10.5281/zenodo.20208987.

That work introduces a conceptual and interpretive account of capital as a historically and structurally embedded system of cognition, decision-making, and institutional behavior. In particular, it establishes the distinction between young thinking and old thinking as cognitive architectures shaping economic agency and capital allocation.

The current paper translates this philosophical system into a formal analytical framework suitable for theoretical decomposition, comparative analysis, and future empirical testing.

The research program therefore operates in two complementary registers:

| Layer | Function |

|---|---|

| Philosophical essay | Narrative ontology and conceptual system |

| Present paper | Formal cognitive and economic model |

This separation allows the underlying ideas to be examined at a higher level of analytical clarity without altering their conceptual content.

Abstract

This paper develops a formal conceptual framework for understanding structural differences between entrepreneurial and institutional investor cognition within modern capitalist systems.

While entrepreneurship research traditionally treats investors primarily as providers of capital for venture creation, this paper argues that institutional investors operate within a distinct cognitive and organizational regime characterized by systemic architectures of risk transformation.

The paper introduces the concept of temporal-strategic cognition, which explains how differences in temporal horizons generate fundamentally distinct forms of economic reasoning, decision-making, and capital allocation. Actors operating under extended temporal horizons integrate cross-domain knowledge, manage uncertainty through portfolio exposure, and prioritize long-term institutional continuity. In this regime, risk is governed not primarily at the level of individual ventures, but at the level of aggregated systems of capital allocation.

Building on this framework, the paper advances a lifecycle-based perspective on industry evolution and examines the critical transition from entrepreneurial formation to institutional stabilization. The central argument is that the institutionalization of capital entails a structural transformation in risk representation and governance — a shift from event-level uncertainty toward distribution-level risk management.

This article serves as the formalization layer of a broader philosophical research program on the evolution of financial cognition and the long-term organization of capital.

Methodological Approach

This paper adopts a conceptual-theoretical modeling approach.

The framework is constructed through synthesis of established research traditions in:

- behavioral economics

- institutional economics

- portfolio theory

- strategic management

- systems and complexity theory

The model is not empirically validated in the present version. Instead, it is formulated as a structured analytical framework intended for subsequent operationalization and empirical extension.

Keywords

Entrepreneurship, Venture Capital, Institutional Economics, Strategic Cognition, Portfolio Theory, Industry Lifecycle, Risk Architecture, Systems Thinking, Capital Allocation

1. Introduction

Entrepreneurship and venture capital are commonly described as complementary functions within innovation ecosystems. Entrepreneurs create firms and technologies, while investors allocate capital to support growth. However, this conventional framing obscures a deeper structural distinction: entrepreneurs and investors operate with different temporal horizons, epistemic frameworks, and strategic objectives.

This paper develops a theoretical model explaining these differences and their consequences for:

- firm development

- industry evolution

- capital allocation

- institutional stability

2. Literature context

Research in entrepreneurship and strategic management has examined:

- entrepreneurial orientation and risk-taking

- venture capital selection and governance

- industry lifecycle theory

- institutional economics and long-term growth

Yet these strands are rarely integrated into a unified framework explaining why founders and investors systematically think differently.

This paper synthesizes:

- entrepreneurship studies

- institutional economics

- strategic management theory

- systems thinking approaches

into a single conceptual model.

2.1 Theoretical synthesis gap: dual rationality in economic cognition

A central limitation in existing literature is the absence of a unified framework distinguishing fundamentally different modes of economic rationality under uncertainty.

This paper integrates four intellectual traditions:

- Behavioral economics (Kahneman): System 1 / System 2 cognition at the decision level

- Portfolio theory: returns as statistical distributions

- Institutional economics (North; Acemoglu): institutional stabilization of uncertainty

- Risk and tail-event theory (Taleb): fat tails and limits of prediction

From this synthesis, we propose two dominant cognitive regimes:

Event-based cognition (entrepreneurial mode)

Decision-making is organized around discrete outcomes, individual ventures, and causal attribution at the project level. Risk is local, immediate, and tied to specific actions.

Distribution-based cognition (institutional investor mode)

Decision-making is organized around statistical ensembles, portfolios, and long-horizon probabilistic structures. Risk is a systemic property of distributions rather than individual outcomes.

This represents not merely behavioral difference but a shift in the epistemic level of economic rationality.

Institutional investors do not simply manage risk better; they operate within a different epistemic regime where uncertainty is transformed through aggregation, diversification, and temporal extension.

3. Temporal-strategic cognition

3.1 Concept definition

Temporal-strategic cognition is defined as:

The cognitive framework through which economic actors perceive time, risk, and system structure when making strategic decisions.

Core proposition:

Different time horizons produce fundamentally different forms of economic rationality.

3.2 Short-horizon cognition (entrepreneurial)

| Dimension | Characteristics |

|---|---|

| Time horizon | Short to medium term |

| Unit of analysis | Venture or product |

| Knowledge depth | Domain-specific |

| Risk perception | Opportunity-focused |

| Success metric | Growth and traction |

Entrepreneurs operate under uncertainty and resource constraints. Their primary function is venture creation and early scaling. This mode is highly effective for innovation but weak in systemic stabilization.

3.3 Long-horizon cognition (investor)

| Dimension | Characteristics |

|---|---|

| Time horizon | Multi-decade |

| Unit of analysis | Portfolio and ecosystem |

| Knowledge depth | Cross-domain |

| Risk perception | Statistical and systemic |

| Success metric | Longevity and dominance |

Institutional investors optimize portfolio-level outcomes across time rather than individual venture performance.

4. Clarification: low-risk strategies as structural transformation of risk

The framework does not describe “low-risk” strategies in the conventional sense of risk aversion or uncertainty avoidance.

Instead, the distinction between entrepreneurial and institutional investor cognition reflects a systemic transformation of risk representation.

Risk is not reduced; it is reconfigured across aggregation levels, time horizons, and epistemic units.

| Dimension | Entrepreneurial cognition | Institutional investor cognition |

|---|---|---|

| Nature of risk | Binary (success/failure) | Distributed (portfolio-based) |

| Core mechanism | Prediction of individual outcomes | Statistical acceptance of distributions |

| Error structure | Idiosyncratic and terminal | Normalized and absorbed |

| Strategic orientation | Single-venture success maximization | Population-level optimization |

This implies a shift:

- from prediction of events

- to governance of distributions

5. Architectures of Risk Transformation: Decomposition of Core Mechanisms

A central conceptual point is that risk transformation cannot be treated as a simple scalar property (i.e., “lower risk”), but must be decomposed into distinct, interdependent operational mechanisms. These mechanisms function together as a composite system, allowing institutional actors to shift from localized event-risk to systemic risk governance.

5.1 Statistical Risk Dilution through Portfolio Aggregation

By spreading exposure across a large and heterogeneous portfolio of ventures, institutions significantly reduce the impact of idiosyncratic failures. Individual losses are absorbed into the aggregate performance, turning what would be catastrophic for a single venture into statistically manageable variance at the portfolio level.

5.2 Temporal Risk Smoothing via Extended Horizons

Multi-decade investment horizons fundamentally alter risk perception. Extended timeframes reduce sensitivity to short-term volatility and allow long-run convergence dynamics, mean reversion, and compounding effects to dominate. What appears highly risky in a 3–5 year window often becomes far more predictable and manageable over 15–30 years.

5.3 Institutional Risk Absorption through Organizational Design

Institutions do not merely manage risk — they embed it within their organizational architecture. This is achieved through sophisticated governance structures, compliance systems, internal diversification, substantial capital buffers, and professional risk committees. Risk becomes institutionally distributed rather than personally borne.

5.4 Selection and Filtering Mechanisms (Venture Screening)

Pre-investment processes — including rigorous due diligence, staged financing, syndication, and expert screening — systematically reshape the incoming distribution of opportunities. These filters truncate the left tail of the risk distribution before capital is deployed, fundamentally improving the quality of the opportunity set.

5.5 Synthesis

Taken together, these mechanisms create a powerful composite architecture of risk transformation. Statistical aggregation reduces variance, temporal extension dampens volatility, institutional design absorbs shocks, and selection processes pre-shape distributions. The result is not the elimination of risk, but its qualitative reconfiguration — from acute, binary, and personal to diffused, statistical, and systemic.

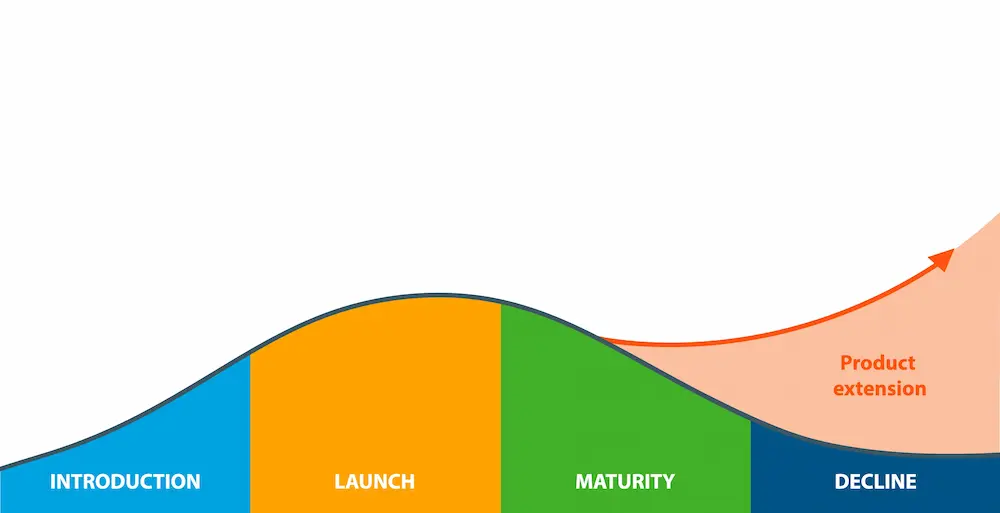

6. Industry lifecycle and firm emergence

Industries evolve through stages:

- Emergence

- Expansion

- Consolidation

- Maturity

Key observation:

Large firms rarely originate in mature industries. They emerge in early phases and later consolidate dominance.

Implications:

- acquisition waves

- platform monopolization

- venture scaling dynamics

7. Founder–institution transition problem

A recurring structural issue is the transition from entrepreneurial leadership to institutional governance.

- Entrepreneurial skills: exploration, experimentation, uncertainty navigation

- Institutional skills: governance, stability, systemic coordination

This mismatch represents a key but under-theorized scaling risk.

8. Knowledge accumulation and institutional memory

Long-term capital depends on:

- accumulated datasets

- historical pattern recognition

- intergenerational learning

Institutional investors operate in historical time rather than operational time.

This produces advantages:

- cycle recognition

- pattern-based decision-making

- systemic risk awareness

9. Implications

Entrepreneurship research

Need to separate venture creation from institutional stabilization.

Venture capital

Evaluation must include cognitive transition potential of founders.

Policy

Innovation systems require both startups and institutions capable of long-term capital accumulation.

10. Conclusion (Final assessment)

The paper does not describe “low-risk” strategies in the conventional sense.

Instead, it describes a transition from individual-level risk management to system-level risk architecture governance within institutional capitalism.

The key analytical shift is not risk reduction but risk reconfiguration across scale, time, and institutional embedding.

The core idea is not “low risk,” but:

a transformation in the nature of risk through scale, temporal extension, and institutional structure

Risk ceases to be a localized property of individual decisions and becomes a structural feature of economic systems governed by portfolios, institutions, and long-horizon dynamics.

Limitations

The present framework is conceptual and interpretive rather than empirically validated.

Several constructs introduced in the paper — including temporal-strategic cognition and distribution-based risk governance — require operationalization for quantitative testing.

Future research may examine these mechanisms through longitudinal investment datasets, institutional portfolio behavior, and comparative founder-investor decision analysis.

AI-Assisted Writing Disclosure

Generative AI tools were used during the language refinement, structural organization, and editorial preparation of this manuscript.

All theoretical constructs, analytical arguments, conceptual models, and final interpretations remain the sole responsibility of the author.

No AI system was used as an author, co-author, or autonomous research agent.

All AI-assisted outputs were reviewed, validated, and substantially modified by the author prior to publication.